Return-to-risk impact of a 50/50 gold and stocks portfolio

A combined approach

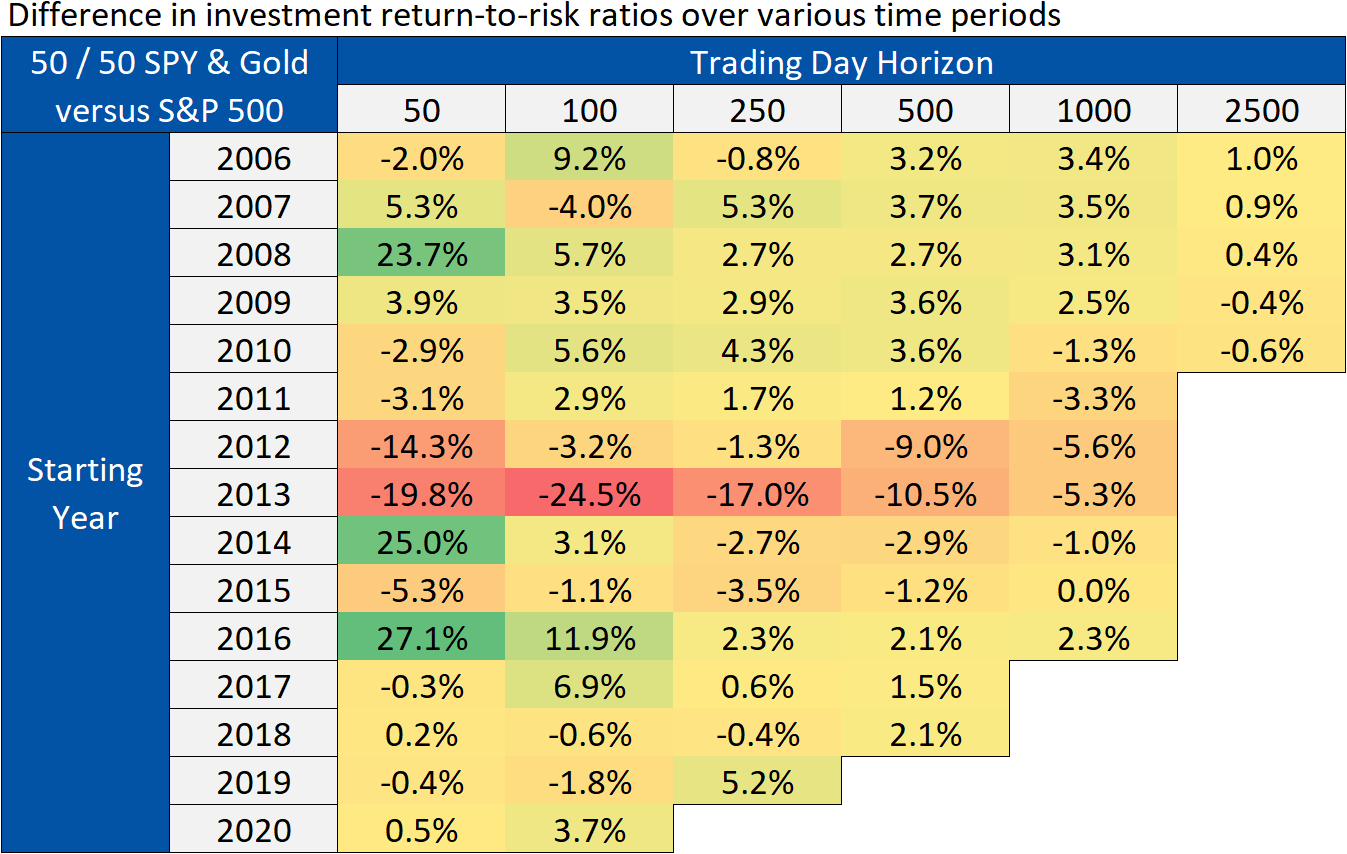

In the last few posts, we looked at the return and risk impact of creating a 50/50 gold (IAU) and stock (SPY) portfolio compared to the S&P 500. To put it altogether, let’s look at the difference between the return-to-risk ratios for the split portfolio and the S&P 500 index over different time periods:

Just like with standard deviation, over the short term, there will be the biggest differences between the portfolio allocations. That smoothes out over time. Unlike standard deviation, the long term benefit isn’t necessarily positive:

There are times it makes sense to hold a split portfolio and times it definitely does not make sense. This isn’t surprising - if it was that easy to just add gold and beat the S&P 500 then everyone would do it. The important thing is that we know gold can be a powerful addition to our portfolio if we allocate properly and at the right time.

Unfortunately, we can’t use the past to predict the future. We are going to have to make a guess on how much gold to allocate to our portfolio right now. (At least we know it will be greater than zero percent!) But, before I make that allocation guess I want to put together a bit more analysis, so we aren’t done with gold just yet.