Solver

Finding optimal solutions

When it comes to finding optimal portfolio allocations, we know that the problem becomes extremely complex very quickly when new investment options are added. Since it can become impossible to calculate every option, Monte Carlo Simulation provides a way to reduce computational cost with an optimality trade off.

But what if you want it all? You want to find the best portfolios at a significantly reduced computational cost. It sounds almost too good to be true:

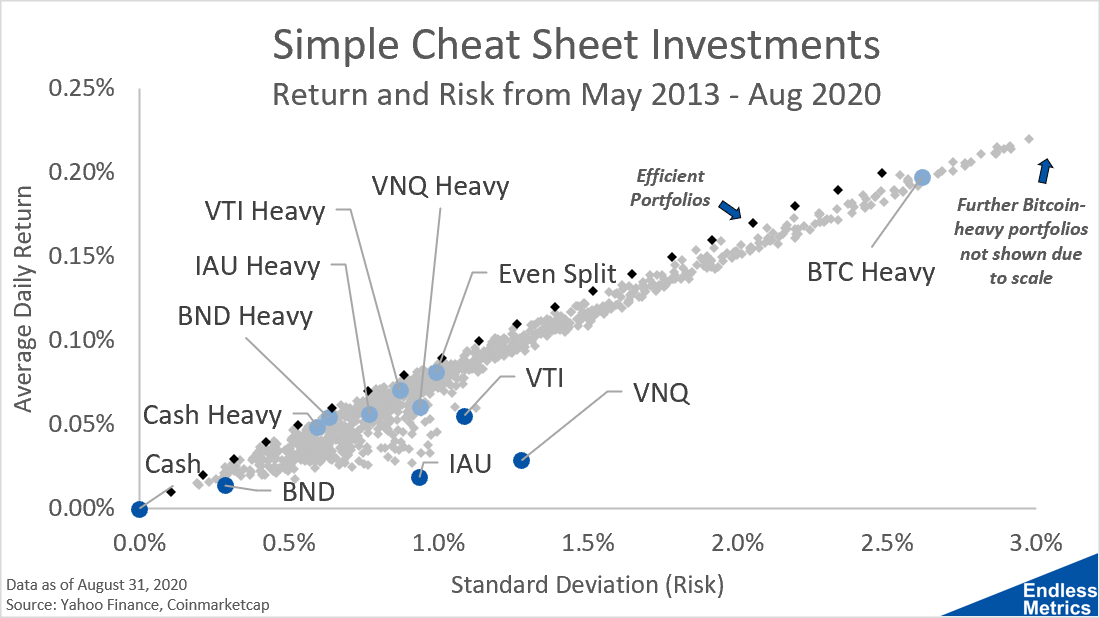

Using the GRG nonlinear approach offered by the Solver add-in within excel, I was able to quickly calculate the efficient portfolios in the chart above. The best part is, for any given return amount I chose, I knew I was getting the portfolio with the smallest amount of standard deviation. These are the absolute best portfolios possible!

Portfolio allocation is just one of the many optimization problems that can be solved by these kinds of algorithms. What’s nice is, once you know how they work, you can learn how to structure problems in a way to use this application to solve them. It’s a great tool for the toolkit. And, it’s really easy to learn.

I think the how-to is covered pretty well elsewhere so I won’t talk about that here. In the next post, we will look at the composition of these “best” portfolios to see what else we can learn about the efficient frontier.