Stock Price, Market Capitalization, and Total Return

There is more to value than just a stock’s price

When people think about stocks, they usually focus on price. However, there is a lot more going on that may not seem very important at first but adds up over time to make a big difference.

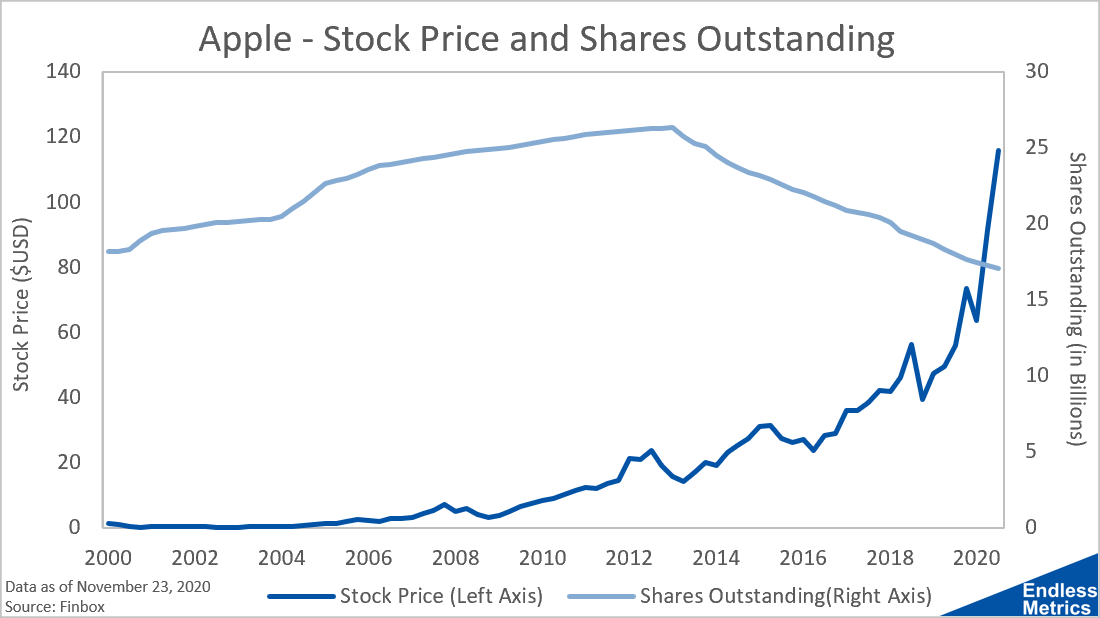

Let’s start by considering not just the price of a stock but also how many shares are available to purchase. Using Apple as an example, everyone knows their stock price has gone up like crazy to make them the world’s most valuable company. At the same time this was happening, the number of shares outstanding steadily decreased for the last seven years or so:

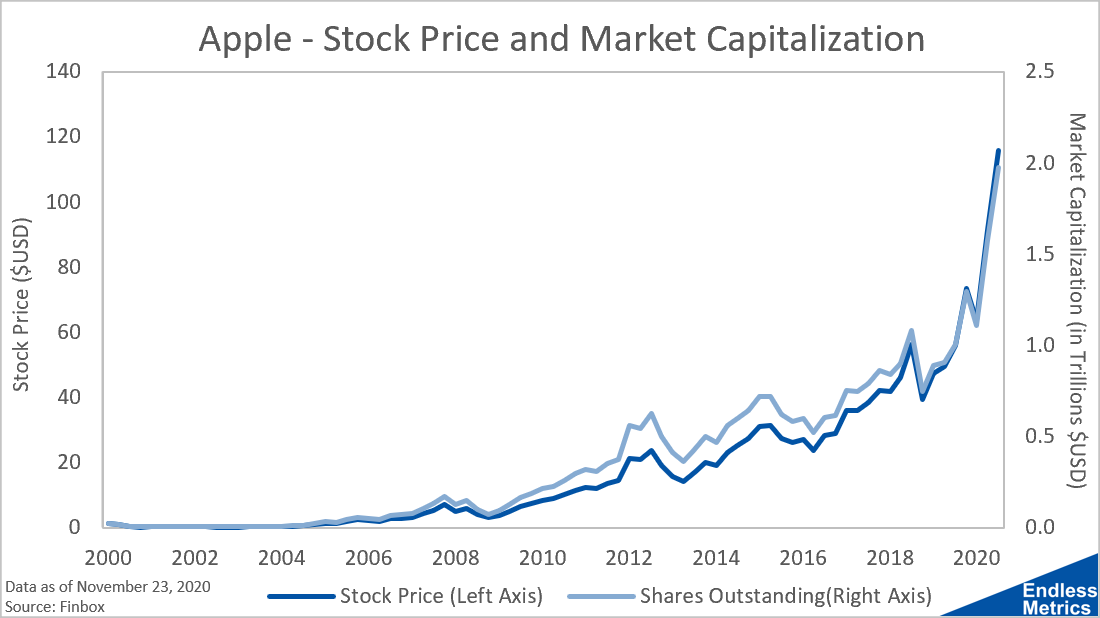

If you multiply shares outstanding with stock price, you get market capitalization. This is what people use to estimate a company’s total valuation. It’s what you’d have to pay to buy the entire company (i.e. purchase every outstanding share available in the stock market). If the stock price is going up but the number of shares is changing, then the total value of the company may be different than the stock price suggests:

That doesn’t appear to be a big difference. But, we can see some variation which means that the value of an individual holder’s shares can diverge from the whole of the company.

This share value difference is also exacerbated by dividends. If an Apple shareholder always reinvested dividends, then the share price would also need to be adjusted to account for this:

With this chart, it really doesn’t look like there is much difference in reinvesting dividends or not. However, these charts, while totally valid, don’t show the true impact of these small cumulative value advantages over the long run.

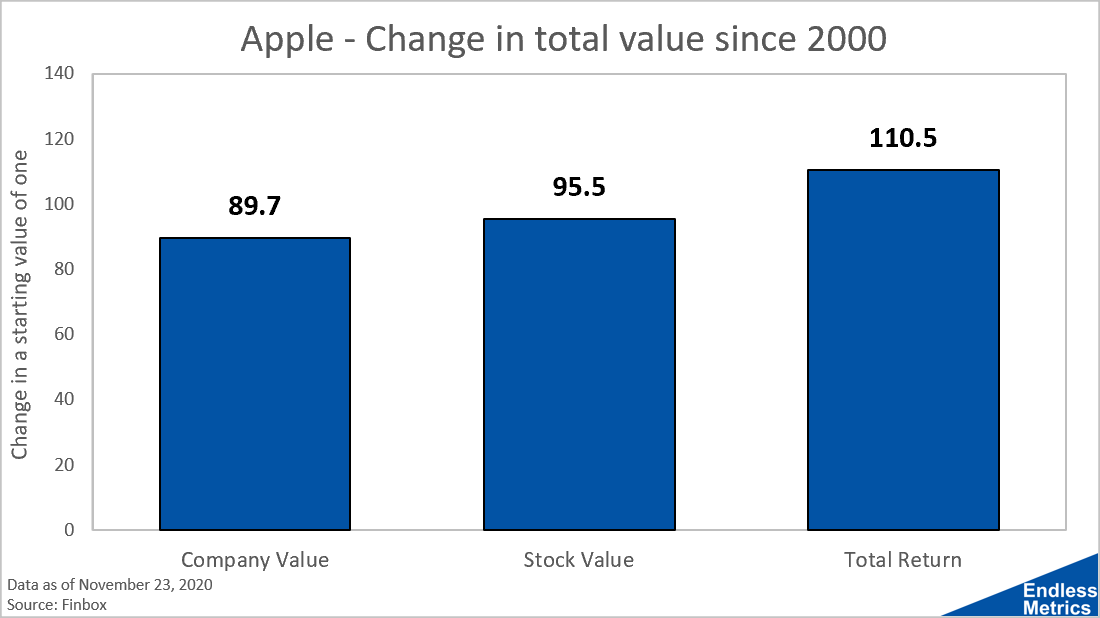

To see the true picture, let’s consider the change in one dollar since 2000 if benchmarked off the market capitalization of Apple, the share price of Apple, and the adjusted share price of Apple when dividends are reinvested:

Now we see a bigger impact. Apple’s value as a total company is 89.7 times bigger than it was in 2000. But, as a shareholder, your investment would be 95.5 times bigger. And, if you had reinvested dividends, 110.5 times bigger! Though, I suppose if one person gets a 90-fold return and another gets a 110-fold return, whats a 2,000% return difference between friends?

While this is just one particular example and is analyzed over a long time period, this phenomenon is critical to understand, as what appear to be insignificant return differences can snowball over time and add up to serious return advantages.

Links

Yesterday’s Post | Most Popular Posts of All Time | All Historical Posts | Contact

One of my favorite articles so far. Nice analysis!